Subsidized vs. unsubsidized federal loans

www.degreechoices.com is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

The U.S. Department of Education offers low-interest subsidized and unsubsidized student loans to help cover the cost of higher education. Both types of loans are part of the William D. Ford Federal Direct Loan Program. Only students who demonstrate financial need are eligible for subsidized loans, which offer better payback terms.

Subsidized and unsubsidized loans account for 52.8% of all federal student loan debt. Of this, 18.6% is in subsidized and 34.2% in unsubsidized loans. The government ensures that interest rates on federal student loans do not exceed 8.25%.

Limits on federal student loans

The annual limit on federal student loans for first-year undergraduates is $5,500.

No more than $3,500 of this amount may be in subsidized loans. This means that a student who qualifies for the full $5,500 their first year can receive up to $3,500 in subsidized loans and the remaining $2,000 would be unsubsidized.

Popular online programs

www.degreechoices.com is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

Interest on subsidized vs unsubsidized loans

Direct Subsidized Loans do not accrue interest until 6 months after you leave school as long as you maintain at least half-time student status.

Direct Unsubsidized Loans begin accruing interest immediately and continue to do until either paid back in full or forgiven. However, you can choose to wait until 6 months after leaving school (your “grace period”) to begin paying interest. The interest you haven’t paid will be added to your principal loan amount (i.e., capitalized).

You can opt out of the grace period if you want to begin making payments sooner, and even make payments while still a full-time student to keep the interest at bay.

What is a Stafford loan?

“Stafford loan” is a term some schools today use to refer to Direct Subsidized Loans and Direct Unsubsidized Loans. Originally, the term was used to distinguish between Direct loans and FFELP loans (which no longer exist).

Managing a Federal Direct Unsubsidized Loan during college

Ideally, make payments while still in school and during the grace period. To help you generate the additional cash needed:

- Consider a part-time job or a work-study program; you can allocate a portion of your earnings towards unpaid accrued interest.

- Calculate how much interest is likely to accumulate each school year; save enough money from your summer job to make interest-only payments throughout the year.

How interest accrues on unsubsidized loans

Below is an example of how much interest would accrue from a loan disbursement August 1st of freshman year through graduation on May 31st, assuming a 5% interest rate.

| Fall 2021 | 2022 | 2023 | 2024 | Spring 2025 | |

| Weighted interest rate based on # of days | 2.10% | 5.00% | 5.00% | 5.00% | 2.07% |

| Unpaid accrued interest | $523.97 | $1,250.00 | $1,250.00 | $1,250.00 | $517.12 |

Repaying your federal student loans

The future impact of loans on your financial wellbeing can be assessed on the basis of 4 main factors:

- Income-earning potential

- Repayment plan

- Marital status/tax-filing status

- Asset allocation

Here, we’ll focus on repayment plans.

Ask yourself the following questions before choosing a repayment plan:

- Am I expecting to pay back my loans in full and how will that affect my cash flow?

- Do I qualify for loan forgiveness, whether this be Public Service Loan Forgiveness (PSLF) or time-based forgiveness?

- Am I focused on trying to reduce my payment to better manage my budget?

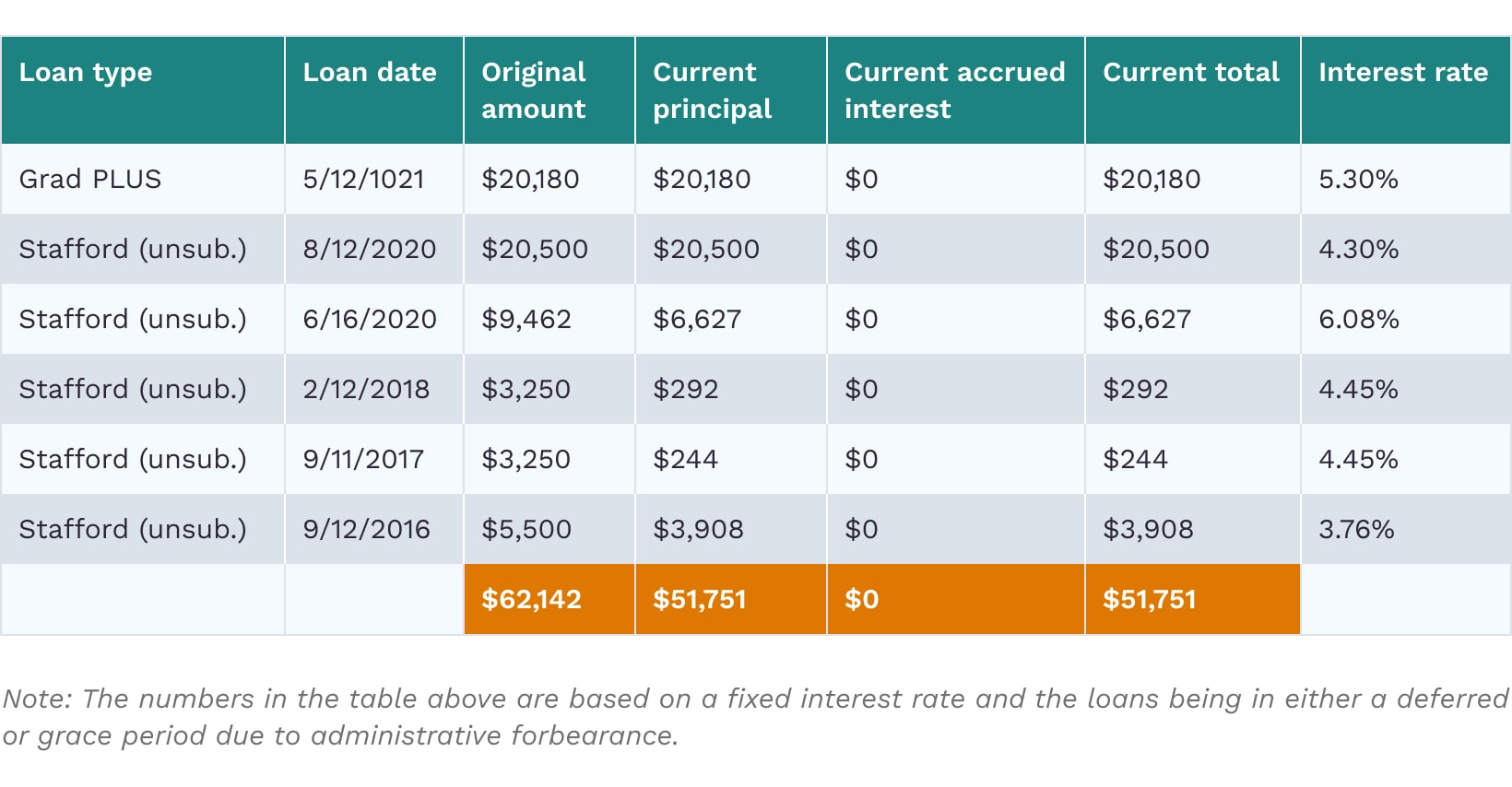

Loan repayment case study

A 24-year-old making $49k per year before taxes has roughly $51,751 in federal loans made up of 5 Direct Unsubsidized Loans and 1 Direct PLUS Graduate Loan.

The individual went to grad school immediately following their bachelor’s. Their parents made payments toward the interest and loans while the individual was in school (during both their undergraduate and graduate studies). They are now looking to take on the burden themselves and make a loan repayment plan.

Option 1: 10-year standard repayment

The most efficient way to pay back their loans would be a 10-year standard repayment:

- The loan servicer would take the current outstanding balance (principal + accrued interest) as well as the number of repayment years and the weighted average of the loan interest rates to calculate a fixed monthly payment. (This is similar to how mortgage payments are calculated.)

This approach tends to offer the best value in terms of total interest paid long term. But what’s the actual damage? According to this scenario, the lender starts paying off their loan in 2022, making monthly payments of $543. By the end of the first year, they would have outstanding debt of $47,709.60.

| Year | Projected monthly | Total outstanding |

| 2023 | $543 | $43,267.40 |

| 2024 | $543 | $38,714.50 |

| 2025 | $543 | $33,940.48 |

| 2026 | $543 | $28,934.40 |

| 2027 | $543 | $23,934.40 |

| 2028 | $543 | $18,179.52 |

| 2029 | $543 | $12,405.97 |

| 2030 | $543 | $6,350.79 |

| 2031 | $543 | $0.00 |

Result

Result

The individual pays their loans off in 10 years by making payments of $543/month ($6,516 annually). The total amount they end up paying is $65,604.49, $13,853.49 of which is interest. In this scenario, the borrower would likely have to reign in their spending significantly and may feel overwhelmed by their monthly loan payments.

Option 2: Income-driven repayment (IDR) plan

Option 2 takes into account that the individual works in the public service sector, which means they could work towards Public Service Loan Forgiveness (PSLF). PSLF is a 10-year forgiveness program only available to borrowers that meet all eligibility requirements.

In this scenario, the requirements are that the borrower is on an income-driven repayment (IDR) plan, working full time in the public sector, and accumulates 120 qualifying payments.

They can choose 1 of the 5 available IDR plans. Let’s say the client opts for the Pay-As-You-Earn (PAYE) plan, which offers the following:

- borrower qualifies so long as they can meet the partial financial hardship requirements

- annual payment is based off 10% of household discretionary income

- borrower has the option of excluding their spouse’s income from the payment formula if they file their taxes “married filing separately”

- on subsidized loans, 100% of unpaid accrued interest is covered by the federal government during the first 3 years of repayment after the grace period

Here, the borrower would start paying off their loan in 2022, making a monthly payment of $238. By the end of the first year, their student debt would amount to $51,347.

| Year | Projected monthly | Total outstanding |

| 2023 | $246 | $50,830 |

| 2024 | $254 | $50,192 |

| 2025 | $262 | $49,423 |

| 2026 | $271 | $48,512 |

| 2027 | $280 | $47,448 |

| 2028 | $290 | $46,215 |

| 2029 | $300 | $44,798 |

| 2030 | $310 | $43,184 |

| 2031 | $321 | $41,353 |

Result

The individual ends up paying anywhere from $238 to $321 per month, assuming their income of $49k grows by 3% each year and they file their taxes “married filing separately” (if married).

After making 120 qualifying payments, they end up paying a total of $28,985.41 over the course of the stated time period and receive tax-free Public Service Loan Forgiveness of $41,353.69.

But what if the borrower doesn’t want to pay back over 10 years, doesn’t qualify for PSLF, and wants to reduce their monthly payment?

They could consider time-based forgiveness, where the remaining loan balance is forgiven after either 20 or 25 years’ worth of IDR payments.

The number of required payments (20 versus 25 years) depends on their IDR plan and whether or not they have graduate loans. If we use the same PAYE IDR outlined above, the required period of payments would be 20 years.

The question then becomes, will there be a loan balance remaining after 20 years of payments and will the borrower end up paying more or less than if they had paid the loans back in full?

Let’s see.

| Year | Projected monthly | Total outstanding |

| 2032 | $332 | $39,289 |

| 2033 | $334 | $36,970 |

| 2034 | $356 | $34,375 |

| 2035 | $369 | $31,477 |

| 2036 | $382 | $28,246 |

| 2037 | $396 | $24,646 |

| 2038 | $410 | $20,627 |

| 2039 | $425 | $16,115 |

| 2040 | $441 | $10,962 |

Result

Their monthly payments will range from $238 to $441 per month, assuming an annual income of $49k with an annual salary increase of 3%.

After 20 years, they have paid a total of $56,286.51 and receive time-based loan forgiveness of $10,962.83. As of right now, federal student loans forgiven prior to 2025 are 100% tax-free.

Final thoughts

We showed you 3 loan repayment scenarios. The first involved a somewhat restricted lifestyle that could impede wealth-building and financial milestones like purchasing a home. The 2 options in the second scenario allow for far more flexibility and control of cash flow while still addressing the student loans. The results of these scenarios demonstrate the importance of financial literacy and understanding your student loans.

www.degreechoices.com is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

Did you enjoy this post?

Related Articles

Continue with these related posts, or visit our blog for comprehensive guides on everything from choosing the right degree to mapping out a career path in your field.