How to pay off student loans fast

www.degreechoices.com is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

Total U.S. student loan debt now stands at $1.748 trillion. This amounts to 43 million borrowers, with an average debt of $37,667. Fifteen percent of all American adults have undergraduate debt, and 7% report outstanding postgraduate loans.

The annual 5-year debt growth rate is 3.79%, making it crucial to begin loan planning as early as possible. Get organized and make the right decisions and you can massively reduce the time it takes to clear the debt.

How long does it take to pay off student loans?

This largely depends on the type of loan, amount borrowed, and repayment schedule. The U.S. department of education indicates that 10 years is the ideal timeline for students to pay off the debt. However, the average borrower takes 20 years.

Funding graduate studies can be more complicated and leads to postgrads opting for loans. In fact, grad students account for around 50% of total outstanding student loan debt. Depending on the subject studied, some professional graduates can take over 45 years to shake off the money owed.

Popular online programs

www.degreechoices.com is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

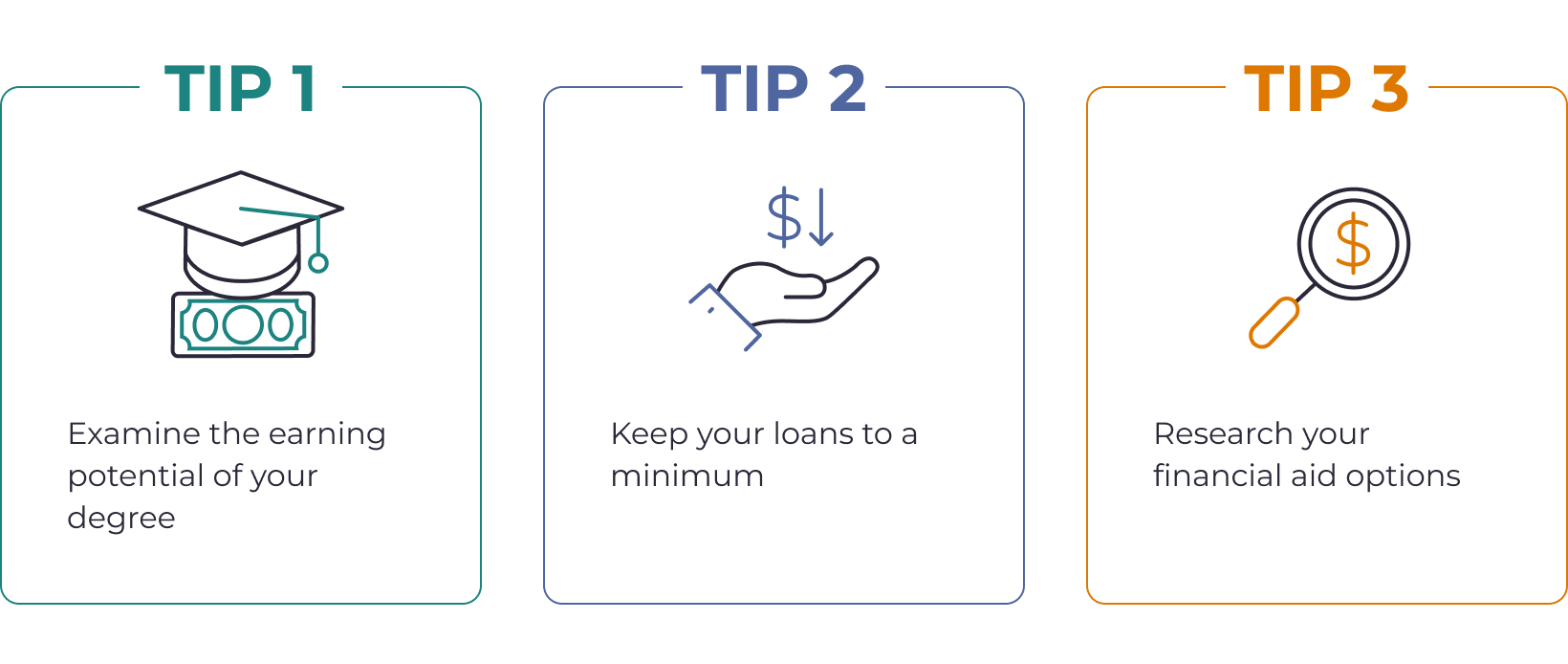

Key tips when first signing up for a loan

Start planning early – debt mitigation can begin before you even set foot on campus. The following tips can significantly decrease the time it takes to repay your student loan.

Tip #1: Consider the ROI of your degree

Getting a degree in a field that does not pay much money can make it more difficult to repay loans quickly. Degrees in engineering, mathematics, and computer science have great placement rates in high-paying positions. Regardless of your eventual major, make sure to choose a program with demonstrated success providing students a good economic return.

Tip #2: Only borrow what you need

Try to borrow only what is needed for vital education-related expenses. Stick to a budget and look at ways to make college more affordable.

Tip #3: Do your due diligence

Avoid signing up for a student loan until you have fully researched the options. Start by filling in the free application for federal student aid (FAFSA) to discover the financial assistance you are entitled to.

If a funding shortfall remains, explore private loan options. The terms tend to be less favorable than the federal alternatives, so compare interest rates and repayment plans from a few different loan providers.

What is the difference between private and federal loans?

Private loans are provided by banks and other financial institutions. Federal loans are provided by the government.

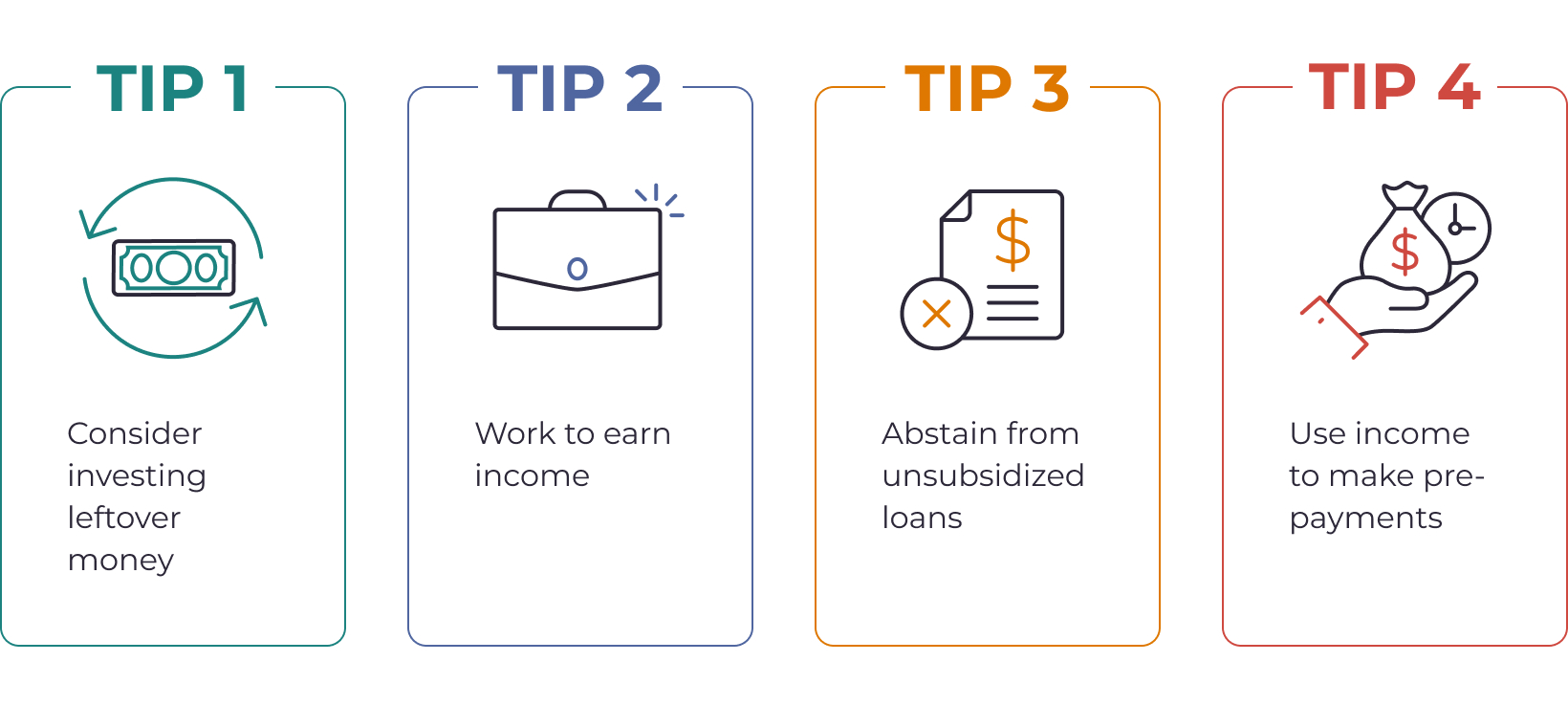

Student loan strategy while in school

At college, your goal should be to keep spending low and earn money to borrow less. Some students get part-time work, others minimize costs by avoiding unsubsidized loans and prepaying if they can.

Tip #1: Minimize discretionary spending and invest

If you have some loan money left over after paying for textbooks, tuition, and supplies, consider investing it. There are a number of relatively low-risk alternatives that might provide a higher rate of return than early prepayment.

Investing always involves an element of risk, but we are not suggesting you take out a student loan and day trade with it. Talk with a financial planner if you are looking to make a large investment.

Tip #2: Get part-time work or enroll in a work-study program

Try to supplement the money you borrow with your own income. Most college campuses offer part-time work opportunities or work-study programs tailored to your schedule and priorities.

Tip #3: Try to avoid unsubsidized loans

Unsubsidized loans accrue interest while you are in college. If you must take out an unsubsidized loan, try to pay the interest off during school.

The table below compares how much a student would owe upon graduation if they took subsidized or unsubsidized loans.

What is the difference between a subsidized and unsubsidized loan?

Students who demonstrate financial need are eligible for a subsidized loan. The U.S. Department of Education pays the interest while the student is at school (and during loan repayment postponement). Unsubsidized loans accrue interest while the borrower is still in college.

Tip #4: Pre-pay whenever possible

If you have additional money from a part-time or summer job, you can use this to make pre-payments on your student loan. This can reduce the future repayments and the amount of interest owed.

On occasion, it might make more sense to invest the money rather than using it to pre-pay because the investment opportunity provides a better return. If you are in a situation where you are unsure which is more beneficial, solicit advice from a financial advisor.

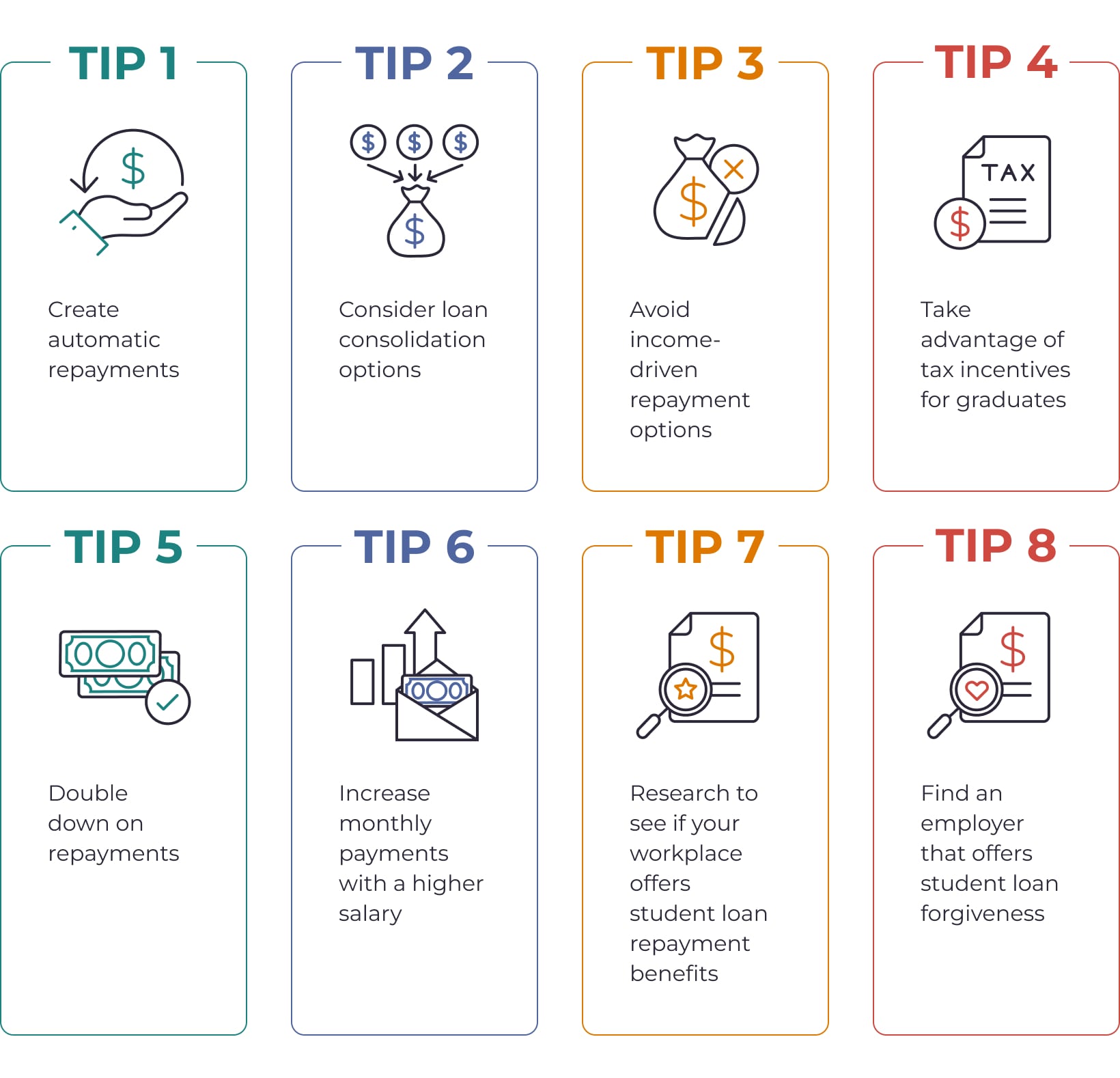

Student loans post-graduation

After graduation, there are several ways to mitigate debt and reduce the time it takes to repay your student loan.

Tip #1: Set up auto-debit to make repayments

Depending on your contract, you may be able to get an interest rate reduction if you agree to payments being automatically taken from your account. Typically, this reduction is 0.25%, which doesn’t sound like much, but can quickly add up.

Tip #2: Explore consolidation options

You may have taken loans from several providers. This can be confusing and makes organizing repayments difficult. Consolidating your loans may be a good idea to make the debt more manageable.

Tip #3: Think twice about income-driven loan repayments

While convenient, an income-driven repayment plan massively increases the time it takes to pay off the loan. In some cases, these plans are unavoidable, but it is worth talking to a financial advisor to see if there are better options available.

Tip #4: Utilize student loan tax incentives

There are several tax incentives that graduates can use to their advantage. These include tax credits and deductions for interest payments. Do some research and talk to a financial advisor about tax break eligibility.

Tip #5: Set up biweekly payments

Instead of making loan payments monthly or even bimonthly (twice per month on specific dates like the 1st and the 15th), consider paying biweekly, or once every 2 weeks. Instead of 12 monthly or 24 bimonthly payments, you make 26 payments per year (52 weeks divided by 2). This adds up to one extra monthly payment every year, meaning you are paying off your principal amount somewhat more quickly and therefore reducing your interest.

Tip #6: Increase your repayment amount if you get a raise

Instead of succumbing to lifestyle creep, consider increasing your repayments whenever you receive a raise. This might not be the most entertaining use of your newfound wealth, but in the long term, you’ll be grateful you made this decision.

Tip #7: Check whether your employer offers a student loan repayment benefit

Many workplaces offer student loan repayment assistance to help attract the best staff. If you’re applying for a job, ask about this benefit during the application process. If you’re already employed, check with human resources to confirm whether this is a company perk.

Tip #8: Get a job that offers loan forgiveness

Some jobs, particularly those in public service, are eligible for loan forgiveness. This means that once you have made a certain number of repayments, the remaining loan balance is cleared. Loan forgiveness is among the quickest ways to pay off your student loans – and may be something to consider when choosing a career.

Final thoughts on paying off student loans fast

There are strategies before, during, and after college that can help you pay back your loans faster. Most importantly, if you are going to borrow money to fund your education, make sure you are considering schools with a track record of providing students good return on their education investment.

www.degreechoices.com is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

Did you enjoy this post?

Related Articles

Continue with these related posts, or visit our blog for comprehensive guides on everything from choosing the right degree to mapping out a career path in your field.